How Oregon Tourism is Structured and Funded by the Transient Lodging Tax (TLT)

Maintaining and promoting tourism requires adequate funding, and in Oregon, like most areas in the US, the main source of revenue for tourism-related initiatives is the Transient Lodging Tax (TLT). In this article we will delve into the details of how Oregon’s tourism industry is structured and funded.

Oregon has a coastline, mountain ranges, deserts and more that attracted over 40 million overnight stays for out-of-state, international and traveling Oregon residents in 2022, (Travel Oregon Report). According to Oregon state law, a visitor is defined as someone who travels more than 50 miles away from their residence or stays somewhere overnight (Oregon Legislature). Oregon’s tourism industry sees $13.9 billion dollars in visitor spending yearly (2022) (Travel Oregon Report).

Structure Breakdown

Marketing efforts to attract visitors to specific areas are conducted by destination marketing organizations (DMOs). DMOs are the organizations that promote and coordinate tourism in their respective area. DMOs often run the visitor center in their municipality. Visitor centers help tourists know what there is to see, eat, and do.

The statewide tourism DMO is Travel Oregon, who works to advance tourism for the entire state of Oregon. The state of Oregon is split into seven regions for tourism, with each region having a regional DMO (RDMO). Each RDMO works to promote tourism in their region, and DMOs work to bring visitors to their specific county or city. Travel Oregon works closely with local DMOs and RDMOs across the state.

It is important to note that DMOs are different from chambers of commerce. A chamber of commerce focuses on advancing local businesses and the economic growth of an area, that includes all businesses including tourism businesses while a DMO focuses on specifically promoting tourism by marketing the destination to visitors. In some areas, the local chamber of commerce may take on the role of a DMO as well. DMOs are funded by the TLT.

Funding Breakdown

The TLT is a specific tax levied on overnight accommodations in Oregon, primarily on hotels, motels, camp sites, vacation rentals and other lodging establishments. It is a tax per room night sold. The TLT is structured at the state, county and city level. At the state level, there is a TLT of 1.5% imposed in addition to a local TLT. The revenue generated from this statewide TLT is used by Travel Oregon for marketing programs, to award competitive grants, and to help fund the respective RDMO (Transient Lodging Tax in Oregon).

At the county and city level, specific local TLT percentages can be established. Overnight visitors are charged either a city level TLT or a county level TLT, but not both. For instance, if a visitor stays overnight in Newport, there is a 12% local TLT imposed within the city limits and if a visitor stays outside of a municipality in Lincoln County, there is a 10% local county TLT applicable (City of Newport & Lincoln County).

In 2018, Oregon saw $12.3 billion in travel spending, state TLT revenue was approximately $40 million Oregon.gov and local TLT yielded $210 million across the state (OPB & ECONorthwest). This tax was first introduced in 2003, aiming to support tourism-related activities. In 2005, the definition of the tax was expanded to include “transient lodging” (Oregon Department of Revenue). A minimum of 70% of the net revenue generated from a new or increased TLT must be dedicated to tourism promotion and tourism-related facilities in the respective city or county. A maximum of 30% of the net revenue may be used to fund city or county services, like transportation infrastructure, parks, and libraries (League of Oregon Cities). This funding mechanism ensures a source of financial support for tourism marketing efforts at both the state and local levels.

Transient lodging providers, such as hotels, have the responsibility of collecting and remitting the tax to the Oregon Department of Revenue on a quarterly basis. To account for associated costs with record keeping, reporting, and collection, Oregon allows a 5% deduction from the state lodging taxes collected by the lodging establishment. (Oregon Department of Revenue). Due to the high level of local TLT variability, reach out to local authorities for city or county TLT rates.

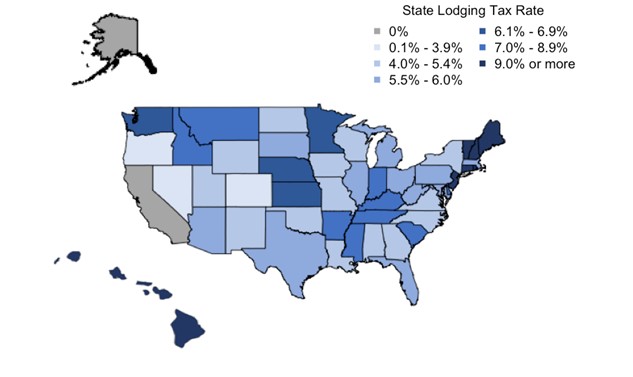

Oregon has a comparatively low statewide lodging tax rate of 1.5% , whereas Connecticut boasts the highest statewide lodging tax rate in the United States at 15% but prohibits the levying of additional lodging taxes locally (Hotel Online). The map below from 2021 shows the state lodging tax rate nationwide, 46 States have a higher state lodging tax rate than Oregon.

Map from Hotel Online.

The TLT has become a vital funding source for Oregon’s tourism industry. Understanding the structure and funding of Oregon’s tourism industry is essential for sustaining and promoting its continued growth and success. For an example of how Oregon is marketed to visitors watch this video, made by Travel Oregon.